NCERT Solutions for Class 12 Micro Economics Perfect Competition

Class 12 Economics textbook solutions Micro Economics Chapter-10 Perfect Competition will give students an advantage with practical questions. NCERT Solutions provided are easy to understand and each step in the solution is described to match student understanding. CBSE Class 12 Economics NCERT Solutions are curated by subject experts and students can rely on these to score well. NCERT Solutions Economics is prepared as per the latest CBSE Syllabus and you can use them during your homework or for your preparation.

Do you want to score high marks in economics in class 12 CBSE board Exams? Then following NCERT Solutions for Class 12 Economics free PDF can help you do it.

NCERT Solutions for Class 12 Economics guides you through this with utmost precision by offering you easy access to important topics in every chapter – so that you save valuable time right before the exam.

NCERT TEXTBOOK QUESTIONS SOLVED

Question 1. What are the Characteristics of a perfectly competitive market? [3 Marks]

Answer:

- Large number of buyers and sellers

- Homogeneous product

- Free entry and exit of firms

- Perfect knowledge about the market

- Perfect mobility of factors of production

- Absence of transportation and selling cost

Question 2. What is price line under perfect competition? [3 Marks]

Answer :

- The price line shows the relationship between the market price and a competitive firm’s output level,

- The vertical height of the price line is equal to the market price as shown in the given figure.

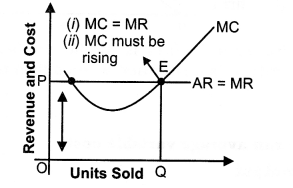

Question 3. What is the relation between market price and average revenue of a price taking firm (i.e. perfectly competitive firm)? [1 Mark]

Answer: The average revenue (AR) of a firm is defined as total revenue per unit of output sold. Let a firm’s output be Q and the market price be P, then TR equals P x Q. Hence,

In other words, for a price-taking firm, average revenue equals the market price.

MORE QUESTIONS SOLVED

I. Very Short Answer Type Questions (1 Mark)

Question 1. Define market for a good. [CBSE 2008]

Answer: Market refers to a region where buyers and sellers of a commodity come in contact with each other to effect the transactions of purchase and sale of the commodity.

Question 2. What are the main forms of market?

Answer: (i) Perfect competition (ii) Imperfect competition.

- Monopoly

- Monopolistic competition

- Oliopolgy.

Question 3. Define perfect competition.

Answer: It refers to a market situation in which buyers and sellers operate freely and a commodity sells at a uniform price.

Question 4. What do you mean by homogenous product?

Answer: Products sold in the market are homogeneous, i.e., they are identical in all respects like quality, colour, size, weight, design, etc.

Question 5. In which market forms are average revenue and marginal revenue of a firm always equal? [CBSE, All India 2004]

Answer: Perfect competition.

Question 6. In which market form does a firm face a perfectly elastic demand curve?

Answer: Perfectly competitive market.

Question 7. What induces new firms to enter an industry? [CBSE Sample Paper 2008]

Answer: Abnormal profits, i.e., above normal profits.

Question 8. If the firms are earning abnormal profits how will the ‘number of firms in industry change?

Answer: The number of firms in the industry will increase.

Question 9. In which market form are goods sold at a uniform price?

Answer: Perfect competition.

Question 10. Why are selling costs not incurred in perfect competition?

Answer: Selling costs are not incurred in perfect competition as there exists perfect knowledge among the buyers and sellers.

Question 11. What is meant by the term ‘price – taker ‘ in the context of a firm?

[CBSE, 2008]

Answer: A firm is said to be a price-taker if it has to accept the price, as determined by the market forces of demand and supply.

Question 12. Under which market form a firm is a price-taker? [CBSE 2004]

Answer: Perfect competition.

Question 13. What is a price taker firm? [CBSE 2012]

Answer: A price taker firm is one which has no option but to accept the price as determined by the industry as in perfect competition.

II. Multiple Choice Questions (1 Mark)

Question 1. What is the shape of the demand curve faced by a firm under perfect competition?

(a) Horizontal (b) Vertical

(c) Positively sloped

(d) Negatively sloped

Answer: (a)

Question 2. Which one of the following equations is not a characteristic of a “price taker”?

(a) TR = P x Q (b) AR = Price

(c) Negatively-sloped demand curve

(d) Marginal Revenue = Price

Answer: (c)

Question 3. Which one of the following options is not a condition of perfect competition?

(a) A large number of firms.

(b) Perfect mobility of factors.

(c) Informative advertising to ensure that consumers have good information.

(d) Freedom of entry and exit into and out of the market.

Answer: (c)

Question 4. Under perfect competition a firm is

(a) price maker and not price taker

(b) price taker and not price maker

(c) neither price maker nor price taker

(d) None of these.

Answer: (b)

Question 5. Which one of the following options is not a characteristic of a perfectly competitive market?

(a) Large number of firms in the industry.

(b) Outputs of the firms are perfect substitutes for one another.

(c) Firms face downward-sloping demand curves.

(d) Resources are very mobile.

Answer: (c)

Question 6. Price-taking firms, i.e., firms that operate in a perfectly competitive market are said to be “small” relative to the market. Which one of the following options best describes this smallness?

(a) The individual firm must have fewer than 10 employees.

(b) The individual firm faces a downward-sloping demand curve.

(c) The individual firm has assets of less than Rs 20 lakh.

(d) The individual firm is unable to affect market price through its output decisions.

Answer: (d)

Question 7. For a price-taking firm.

(a) marginal revenue is less than price

(b) marginal revenue is equal to price

(c) marginal revenue is greater than price

(d) the relationship between marginal revenue and price is indeterminate

Answer: (b)

Question 8. The firm in a perfectly competitive market is a price taker. This designation as a price taker is based on the assumption that

(a) the firm has some, but not complete, control over its product price.

(b) there are so many buyers and sellers in the market that any individual firm cannot affect the market.

(c) each firm produces a homogeneous product.

(d) there is easy entry into or exit from the market place.

Answer: (b)

Question 9. Suppose that a sole proprietorship is earning total revenues of Rs 1,00,000 and is incurring explicit costs of Rs 75,000. If the owner could work for another company for Rs 30,000 a year, we would conclude that—————-

(a) the firm is incurring an economic loss.

(b) implicit costs are Rs 25,000.

(c) the total economic costs are Rs 1,00,000.

(d) the individual is earning an economic profit of Rs 25,000.

Answer: (a)

Question 10. A purely competitive firm’s supply schedule in the short run is determined by—————-

(a) its average revenue.

(b) its marginal revenue.

(c) its marginal utility for money curve.

(d) its marginal cost curve.

Answer: (d)

Question 11. The term market’ refers to a——————-

(a) place where buyer and seller bargain a product or service for a price

(b) place where buyer does not bargain

(c) place where seller does not bargain

(d) None of these.

Answer: (a)

III. Short Answer Type Questions (3-4 Marks)

Question 1. Explain feature of homogeneous product. [AI2004, 11; CBSE 07, 09C] Or

Explain the implication of : homogeneous product.

Answer:

- Products sold in the market are homogeneous, i.e., they are identical in all respects like quality, colour, size, weight, design, etc.

- The products sold by different firms in the market are equal in the eyes of the buyers.

- Since, a buyer cannot distinguish between the product of one firm and that of another, he becomes indifferent as to the firms from which he buys.

- The implication of this feature is that since the buyers treat the products as identical they are not ready to pay a different price for the product of any one firm. They will pay the same price for the products of all the firms in the industry. On the other hand, any attempt by a firm to sell its product at a higher price will fail.

To sum up, the “homogeneous products” feature ensures a uniform price for the products of all the firms in the industry.

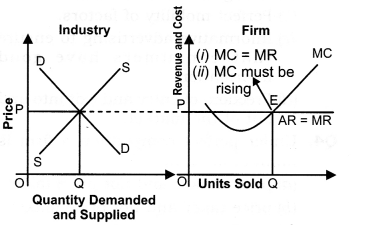

Question 2. “In perfect competition, industry is the price maker and firm is the price taker.” Discuss.

Answer: Yes, this statement is true.

- As we know, in Perfect competition, homogeneous goods are produced. So, industry cannot charge different price from different firms.

- So, industry will give that price to the firm where industry is in equilibrium, i.e., where Demand = Supply. Any movement from that point would be unstable.

- In the given diagram, price and revenue is measured on vertical axis and units of commodity on horizontal axis. Industry will give OP price or point E to the firm as at that point Demand = supply, i.e., industry is in equilibrium. The firms will follow the same price and charges same from the consumer.

Question 3. Explain features of perfect knowledge about the market.

Answer:

- Perfect Knowledge means both buyers and sellers are fully informed about the market.

- The firms have all the knowledge about the product market and the input markets. Buyers also have perfect knowledge about the product market.

- Let us first take the product market. The implication of perfect knowledge about the product market is that any attempt by any firm to charge a price higher than the prevailing uniform price will fail. The buyers will not pay because they have perfect knowledge. A uniform price prevails in the market.

- Regarding the knowledge about the input markets the implicit assumption is that each firm has an equal access to the technology and the inputs used in the technology.

- No firm has any cost advantage. Cost structure of each firm is the same.

- Since there is uniform price and uniform cost in case of all firms, and since profit equals revenue less cost, all the firms earn uniform profits.

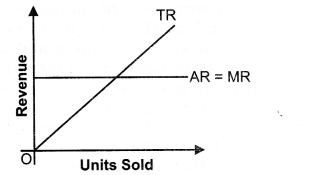

Question 4. What is the relationship between TR, AR and MR under perfect competition?

Answer:

- In the perfect competition, a firm is a price taker.

- It has to sell its product at the same price as given (determined) by the industry. Consequently, price = AR = MR.

- Hence, a firm’s AR and MR curve will be a horizontal straight line parallel to X axis.

- Since price remains the same, i.e., MR is constant, therefore, TR increases at the Constant rate as increase in the output sold.

- As the result of, TR curve facing a competitive firm is positively sloped straight line. Again, because at zero output Total Revenue is zero therefore, TR curve passes through the origin O as shown in the given figure.

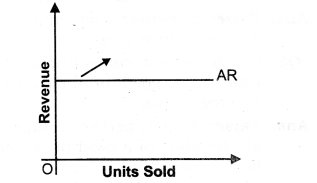

Question 5. Why is AR curve of a firm under perfect competition parallel to X-axis? [CBSE 2006]

Answer:

- AR curve of a firm under perfect competition is parallel to X-axis because in perfect competition homogeneous product are produced, that is why price remains constant and as we know AR = TR/Q = PX Q/Q = Price. So, AR remains constant.

- As, AR is on Y-axis, that is why AR curve remains constant and parallel to X-axis.

Question 6. There are large number of sellers in a perfectly competitive market. Explain the significance of this feature. [CBSE 2015]

Answer: Large number of sellers—:

- The words large number’ simply states that the number of sellers is large enough to render a single seller’s share in total market supply of the product insignificant,

- Insignificant share means that if only one individual firm reduces or raises its own supply, the prevailing market price remains unaffected.

- The prevailing market price is the one which was set through the intersection of market demand and market supply forces, for which all the sellers and all the buyers together are responsible. (iv) One single seller has no option but to sell what it produces at this market determined price. This position of an individual firm in the total market is referred to as price taker. This is a unique feature of a perfectly competitive market.

IV. True Or False

Giving reasons, state whether the following statements are true or false.

Question 1. In perfect competition, a firm independently determines price.

Answer: False: In perfect competition, a firm is only price taker and industry is price maker.

Question 2. In perfect competition every firm of the industry is price maker.

Answer: False: In perfect competition, every firm is a price taker.

Question 3. Under perfect competition, all the units of a good produced can be heterogeneous.

Answer: False: Under perfect competition, all the units of a good produced are homogeneous.

Question 4. The condition for shut down point is, the price is equal to minimum of short run average cost.

Answer: False: It is so because the condition for shut down point is the price equal to minimum of short run average variable cost.

Question 5. In perfect competition, selling costs can help in raising sale of the product.

Answer: False: Under perfect competition, as the units of a good are homogeneous and are sold at the same price.

Question 6. Rising portion of MC curve is a supply curve of a competitive firm.

Answer: False: Supply curve is that part of rising MC curve which would be greater than or equal to minimum of short run average variable cost.

Note: As per CBSE guidelines, no marks will be given if reason to the answer is not explained.

V. Long Answer Type Questions (6 Marks)

Question 1. Explain feature (implication) of ‘large number of sellers and buyers’ in perfect competition. [CBSE 2005C, 10, IOC, 11C; AI 08, 10, 11, 13] Or

Explain the implications of large number of sellers in a perfectly competitive market.

Or [AI 2012]

Explain the implications of large number of buyers in a perfectly competitive market. [CBSE 2012]

Answer: Large number of sellers—:

- The words ‘large number’ simply states that the number of sellers is large enough to render a single seller’s share in total market supply of the product insignificant.

- Insignificant share means that if only one individual firm reduces or raises its own supply, the prevailing market price remains unaffected.

- The prevailing market price is the one which was set through the intersection of market demand and market supply forces, for which all the sellers and all the buyers together are responsible. (iv) One single seller has no option but to sell what it produces at this market determined price. This position of an individual firm in the total market is referred to as price taker. This is a unique feature of a perfectly competitive market.

Large number of buyers—:

- The words ‘large number’ simply states that the number of buyers is large enough, that an individual buyer’s share in total market demand is insignificant, the buyers cannot influence the market price on his own by changing his demand.

- This makes a single buyer also a price taker.

To sum up, the feature “large number” indicates ineffectiveness of a single seller or a single buyer in influencing the prevailing market price on its own, rendering him simply a price taker.

Question 2. Explain the features of free entry and exit of firms.

[CBSE 2004, 07, 09C] Or

Explain the outcome of the following features of a perfectly competitive market:

[CBSE 2013C, CBSE Sample Paper 2014]

- Freedom to firms to enter the industry.

- Freedom to the firms to leave the industry.

Answer:

- Buyers and sellers are free to enter or leave the market at any time

they like. New firms induced by large profits can enter the industry whereas losses make inefficient firms to leave the industry. - The freedom of entry and exit of firms has an important implication. This ensures that no firm can earn above normal profit in the long run. Each firm earns just the normal profit, i.e., minimum necessary to carry on business.

- Suppose the existing firms are earning above normal profits, i.e. positive economic profits. Attracted by the positive profits, the new firms enter the industry. The industry’s output, i.e. market supply, goes up. The prices come down. New firms continue to enter and the prices continue to fall till economic profits are reduced to zero.

- Now suppose the existing firms .are incurring losses. The firms start leaving. The industry’s output starts falling, prices going up, and all this continues till losses are wiped out. The remaining firms in the industry then once again earn just the normal profits.

- Only zero economic profit in the long run is the basic outcome of a perfectly competitive market.

VI. Higher Order Thinking Skills

Question 1. What are the conditions for short run shut down point? [1 Mark]

Answer: Price = minimum of SAVC (short run average variable cost)

Or TR = TVC

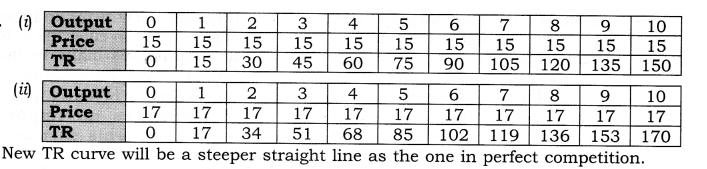

Question 2. A perfectly competitive firm faces market price equal to Rs 15. [3-4 Marks]

(i) Derive its total revenue schedule for the range of output from 0 to 10 units.

(ii) Suppose the market price increases to 17. Will the new TR curve be flatter or steeper?

Answer:

VII.Value Based Questions

Question 1. What is a competitive market? Briefly describe a type of market that is not perfectly competitive. [3 Marks]

Answer:

- A competitive market is a market in which there are many buyers and many sellers of an identical product so that each has a negligible impact on the market price.

- Another type of market is a monopoly in which there is only one seller.

- There are also other markets that fall between perfect competition and monopoly i.e. monopolistic competition.

Value: Analytic

Question 2. What is the relationship between a perfectly competitive firm’s marginal cost curve and its short-run supply curve? [ 1 Mark]

Answer: The marginal cost curve of a perfectly competitive firm is the firm’s short- run supply curve at the point where price is equal to or greater than average variable cost. To determine its quantity supplied the firm equates the price of its product with its marginal cost.

Value: Analytic

VIII.Application Based Question

Question 1. “The rising portion of the SMC curve is the firm supply curve of competitive firm”. Explain.

Or

Explain the short run supply curve of the firm. [6 Marks]

Or

‘Supply curve is the rising portion of marginal cost curve over and above the minimum of Average Variable cost curve’. Do you agree? Support your answer with valid reason. [CBSE Sample Paper 2016]

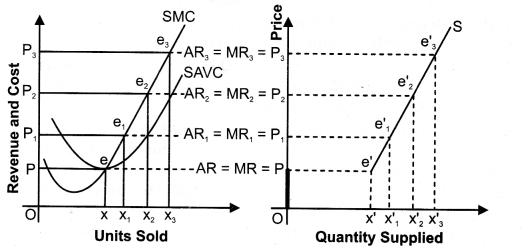

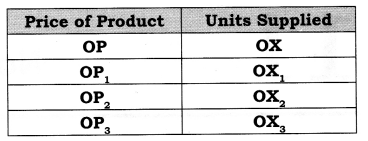

Answer:

- The supply curve of the firm tells us the quantity of the product that a firm is willing and able to produce and sell at each possible price.

- The firm will produce and supply an output at the point at which Price is equal to Marginal cost. The derivation of the supply curve is explained with the help of the given figure.

- The SMC of the firm is given. Let us initially assume that the market price is OP1 . The firm will produce and supply an output of OX1 because at e1, price = MC. (OX1 is the equilibrium output supplied, as MC = MR and MC cuts MR from below).

- Suppose the market price rises to OP2, then the firm will produce and sell OX2 level, because at e2 level price = MC = MR.

- Similarly, as market price increases to OP3, quantity supplied increases to OX3. However, the firm will not supply any quantity if the price falls below OP.

- At OP price, the firm will produce and sell OX output. For any price below OP the firm will not produce and sell anything. The supply will be zero units. Having the above information, the supply schedule can be determined as,

- If the market price falls below the minimum of the SAVC, the supply curve jumps to the small segment (OP) on the vertical axis at which there is zero supply. Therefore, two discontinuous [(OP) + (e’S)] pieces define the short run supply curve for the perfectly competitive firm.

0 Comments

Please Comment